The SA Reserve Bank and the National Democratic Revolution

On 30 June 1921, the South African Reserve Bank was established in terms of the Currency and Banking Act, 1920 (Act No. 31 of 1920) in the Union Parliament. This came into being after a Gold Conference was held in October 1919. Prior to its establishment South African commercial banks issued banknotes to the public, as they had to convert the notes from the public in to gold. Subsequently the gold was sold to London, and the gold had to be re-imported into South Africa and then be converted into banknotes again.

The commercial banks then requested the government to release them from the obligation to convert their banknotes into gold on demand. For this reason, the Gold Conference was convened to discuss South Africa’s currency. During the conference a Select Committee of the Parliament recommended the establishment of a central bank to take over the gold held by commercial banks and the issuing of banknotes. The recommendation was accepted by the South African Parliament. The South African Bank opened its doors for business on 30 June 1921.

The South African Reserve Bank (SARB) was established on 30 June 1921 as a privately owned public company, a structure it largely maintains today, though its governance, regulatory mandate, and operational composition have shifted from commercial representation to constitutional public service. In 1921, the SARB was established with 2 million ordinary shares. By law, South African commercial banks were required to buy shares to fund its launch, alongside private individuals and “stockholders” from the general public. Individual holdings were originally capped at £10,000. Now the SARB remains one of fewer than 10 central banks globally with private shareholders. However, commercial banks are no longer required to hold shares.

There are roughly 800 private shareholders, and individual holdings are strictly limited to a maximum of 10,000 shares. Ownership is purely “notional”, meaning that Shareholders have no say over monetary policy, financial stability or the appointing of governors. Dividends are legally capped at a maximum of 10 South African cents per share annually, with 90% of remaining surplus profits paid directly to the South African government. The shares were delisted from the JSE in 2002 and traded only on an over the counter (OTC) facility. In 1921 the board composition heavily favoured private investors and commercial banking institutions, reflecting the era’s global central banking norms where private markets drove policy. The government appointed only the Governor and Deputy Governor.

Now the board consists of 15 directors and is structured to balance public accountability with sectoral expertise. Eight are appointed by the President of South Africa (after consulting the Minister of Finance). This includes the Governor, 3 Deputy Governors, who serve as executive directors running daily operations, and 4 non-executive directors. 7 are elected by shareholders as non-executive members who represent specific economic sectors. Two are from commerce/finance, two from industry, one from agriculture, one from mining, and one from labour.

The functional composition of the SARB has evolved dramatically from an emergency commercial backstop into a constitutionally bound public institution. The Twin Peaks regulatory system, implemented in South Africa on 1 April 2018 through the Financial Sector Regulation (FSR) Act of 2017, fundamentally reshaped banking supervision by separating the oversight of financial soundness from the oversight of market conduct. Previously, South Africa used a fragmented, sectoral approach where banks and insurers were regulated by completely different entities under separate laws. Twin Peaks replaced this with two dedicated “peaks” that supervised all financial institutions across the board.

The first peak focuses on financial health, capital strength and risk management. It operates as a juristic person housed inside the South African Reserve Bank (SARB) that is chaired by a SARB Deputy Governor. The Prudential Authority (PA) ensures that banks, mutual banks, cooperative financial institutions, and insurers are inherently safe, stable, and adequately capitalised. Previously, the SARB Bank Supervision Department (BSD) only watched banks. The PA now supervises financial conglomerates. If a single corporate group owns both a major bank and a massive insurance firm, the PA supervises the entire group’s combined risk profile to prevent a domino effect.

The second peak focuses entirely on consumer protection, transparency and market integrity. It is an independent regulator located outside the SARB, which completely replaced the old Financial Services Board (FSB). The Financial Sector Conduct Authority (FSCA) regulates how banks treat customers, design products, disclose fees and market their services. Historically, South African banks were largely unregulated for market conduct regarding their actual core banking products. Regulatory oversight mostly covered external intermediary advice or credit provision. Under Twin Peaks, the FSCA actively monitors and enforces the Treating Customers Fairly (TCF) framework directly onto bank product design, structural fairness, and complaints procedures.

The system fundamentally changes daily banking supervision in four ways. Firstly, was from Reactive to Proactive, meaning that regulators no longer just checked compliance against checkboxes. Instead, they take an intrusive, forward-looking, risk-based approach to stop systemic failures before they start. The FSR Act legally bound the SARB to maintain and enhance overall macroprudential financial stability, giving it sweeping new powers over financial market infrastructures like exchanges and clearinghouses.

To operate a bank in South Africa, an institution must satisfy both peaks. A bank can be financially robust (satisfying the PA), but if its fee disclosures or product lines abuse consumers, the FSCA can intervene or penalise it. Financial institutions can no longer abuse regulatory loopholes by hiding complex cross-market products between banking and insurance laws, as both authorities cooperate via legally mandated co-ordination mechanisms.

Looking at the ongoing debate surrounding the structural identity of the South African Reserve Bank (SARB) highlights a fundamental choice between institutional independence and democratic alignment. This tension has been brought to the forefront by parliamentary hearings over proposed nationalisation legislation. An analysis of both structural models reveals specific operational and economic trade-offs. Under the Current Hybrid Model (Privately Owned Public Company), the bank operates as an independent public company with individual, commercial and foreign private shareholders.

The advantages are the insulation from political interference. Private shareholders help serve as a psychological and structural buffer. They ensure that the state does not treat the central bank as an immediate piggy bank or printing press to fund short-term political goals. Because it is a public company, the SARB is legally bound to hold an Annual General Meeting (AGM) and publish audited financials to private stakeholders. This introduces a layer of public accountability separate from state-run reporting lines. By law, shareholders elect 7 non-executive directors who must represent key economic sectors (agriculture, mining, industry, labour and commerce). This directly incorporates diverse sector insights into the governance framework. International markets view this legacy structure as a signal of institutional strength, which helps protect the value of the Rand and stabilises foreign investment.

Despite stringent rules capping individual ownership at 10,000 shares, having a central bank owned by private individuals and foreign nationals, creates a persistent public perception that a vital state asset is serving private interests rather than ordinary citizens. This layout remains a lightning rod for constant ideological conflict, drawing political energy away from broader economic policy focus. Critics argue that private shareholders inherently incentivise a conservative monetary policy focused strictly on inflation targeting rather than aggressive employment creation or structural economic transformation.

Under a proposed State-Owned Entity (Full Nationalisation) system, the South African government would buy out the 2 million private shares, making the state the sole shareholder. Proponents, like COSATU, argue that the state should hold outright ownership of its currency issuer to fully align national monetary policies with state development goals. This change would remove South Africa from a small minority of countries with private central bank shareholders, moving it into alignment with standard international public governance practices. If the Minister of Finance appoints all board directors directly, the executive and monetary functions can work in closer harmony to solve macro-structural economic challenges.

However, the disadvantages are that buying out the current shareholders involves a costly expropriation process. If the compensation rate is legally disputed, it could result in protracted, expensive constitutional court cases. Shifting full board appointment powers exclusively to the Minister of Finance increases the systemic risk of political patronage or ideologically driven management.

Given the historic structural and financial challenges faced by other South African State-Owned Entities (such as Eskom or Transnet), local business groups warn that nationalisation could trigger a downgrade in investor confidence, leading to capital flight and currency depreciation. Critics express concern that a debt-pressured government might attempt to access the SARB’s multi-billion-rand foreign exchange reserve billion-randout ailing state structures, potentially compromising national financial stability.

The state’s top financial institutions – the National Treasury and the South African Reserve Bank (SARB) – have formally concluded that keeping the SARB privately owned is currently the best choice for South Africa. They argue that nationalisation carries deep economic risks with zero practical policy benefits. The physical cost to buy out the shareholders depends entirely on the legal valuation framework used. The SARB currently has 2 million issued shares trading over-the-counter for roughly R10 to R15 each. At face value, buying out all shareholders would cost the state a mere R20 million to R30 million. If this were the only cost, nationalisation would be highly affordable.

Some private shareholders argue they are entitled to a share of the SARB’s massive internal contingency reserves and cumulative assets if bought out. If courts side with them, the required payout could skyrocket into billions of Rands. Legislative drafts like the SARB Amendment Bill have proposed seizing the shares for zero compensation. While this removes the immediate cash cost, it triggers severe long-term institutional damage. National Treasury actively opposes nationalisation because the true financial burden is not the cost of the shares, but the negative economic fallout it could trigger.

Many SARB shareholders are foreign nationals. Forcing them out without market-value compensation violates international bilateral investment treaties, opening South Africa up to expensive, protracted international litigation. Global investors view the SARB’s unique private shareholding structure as a psychological shield guaranteeing its independent policy. Removing it sparks fear of state interference, potentially leading to bond-market sell-offs, capital flight and a weaker Rand. If investor confidence drops, South Africa’s sovereign risk premium rises. Even a tiny tick upward in state interest rates will cost the country billions more annually to service its national debt.

The most compelling argument against nationalisation is that it spends financial and political capital to achieve no functional change. The SARB’s objective – protecting the value of the currency through inflation targeting – is written directly into Section 224 of the Constitution. Changing the shareholders does not change the Constitution. The state already selects the Governor and all Deputy Governors. Private shareholders have zero say over repo rates, money printing or banking regulations. Shareholders receive a strictly capped total dividend pool of just R200,000 per year. The rest of the SARB’s surplus profits (90%) are already paid directly to the South African government.

Ultimately, while state ownership matches global norms, executing it in South Africa introduces heavy macroeconomic risks for purely cosmetic structural changes. The view that the South African Reserve Bank’s (SARB) current structure is a “neo-colonial” arrangement that disadvantages society is a prominent argument within South Africa’s socio-economic debates. It is a central viewpoint held by political parties like the Economic Freedom Fighters (EFF), trade union federations like COSATU, and various economic oversight factions. At the same time, institutional economists, the National Treasury, and international investors argue that the bank’s structure is a standard modern framework designed to protect the poor from hyperinflation.

To understand why this issue is so deeply contested, it helps to break down both sides of the argument regarding the SARB’s mandate, unemployment and the banking sector. Critics who label the arrangement as neo-colonial or counter-productive point to several structural factors. Proponents of this view argue that strict inflation targeting – keeping inflation between 3% and 6% by raising interest rates – is a policy copied from developed Western economies. They argue that in a country with a 30%+ unemployment rate, the central bank’s absolute priority should be job creation and economic growth, not just price stability.

By remaining completely independent and insulated by a hybrid ownership model, the SARB cannot be compelled by the ruling government to print money or directly fund state development projects, infrastructure, or state-owned enterprises (quantitative easing). Critics see this as an artificial constraint on sovereign economic power. South Africa’s banking sector is heavily dominated by a few massive commercial banks (the “Big Five”). Critics argue that the SARB’s strict prudential and capital regulations – modelled on international standards like Basel III – create exceptionally high barriers to entry. This makes it incredibly difficult for smaller, black-owned, community or cooperative banks to establish themselves and lend to under-serviced areas.

Conversely, the National Treasury, the SARB executive, and mainstream economists argue that the current mandate is actually the best protection South African society has, specifically for the poorest citizens. The SARB argues that its focus on price stability is inherently pro-poor. Wealthy individuals can buy assets (shares, property) to protect their wealth from inflation, whereas low-income earners rely entirely on cash wages. If the SARB abandoned inflation targeting to chase short-term growth, runaway inflation would erode the buying power of ordinary citizens and social grants, worsening poverty.

Defenders of the bank point out that Section 224(1) of the South African Constitution does not isolate inflation. It states: “The primary object of the South African Reserve Bank is to protect the value of the currency in the interest of balanced and sustainable economic growth in the Republic”. The SARB’s position is that sustainable job creation is impossible without a stable currency and predictable economic foundation. Regarding small banks, the SARB and the Prudential Authority argue that strict regulations are not meant to block competition, but to protect depositors. South Africa’s history, such as the collapses of VBS Mutual Bank or African Bank, shows that when small banks fail due to weak regulations or poor governance, it is ordinary, working-class depositors and municipalities that lose their money.

A critical nuance in this debate is that the SARB’s mandate has nothing to do with its private shareholders. The private shareholders have zero legal power to set, alter or vote on monetary policy or regulatory mandates. The SARB’s mandate is dictated entirely by the Constitution of South Africa, which was written and adopted democratically in 1996. Therefore, if South Africa wanted to compel the SARB to focus directly on unemployment or force it to relax rules for community banks, buying out the private shareholders would not achieve this. Parliament would have to pass a Constitutional Amendment to change Section 224.

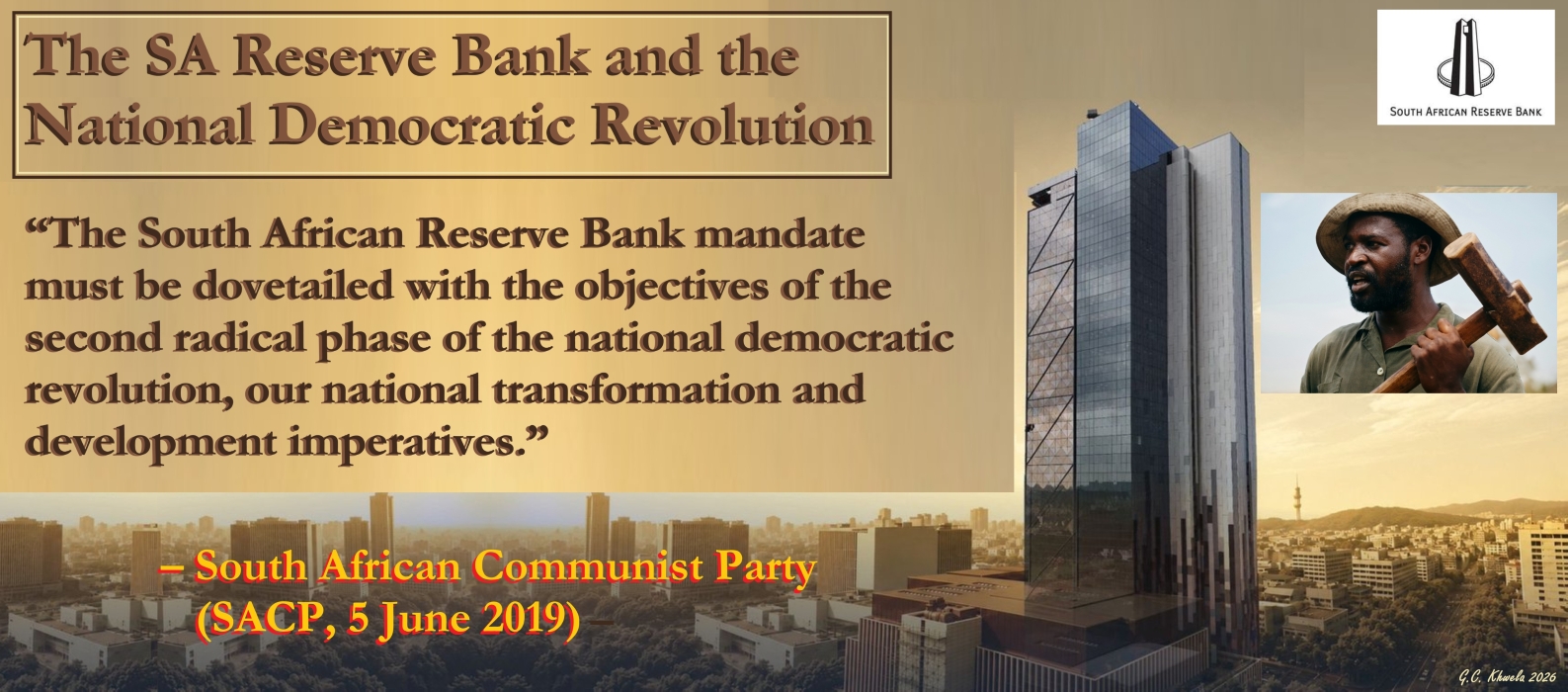

The South African Communist Party (SACP) argued on 5 June 2019, that “the South African Reserve Bank mandate must be dovetailed with the objectives of the second radical phase of the national democratic revolution, our national transformation and development imperatives.”

Sources:

South African History Online (SAHO).

Financial Regulatory Reform Steering Committee, “Implementing a Twin Peaks Model of Financial Regulation in South Africa”, Financial Regulatory Reform Steering Committee, 1 February 2013.

Jannie Rossouw, “Should Central Banks Have Private Shareholders?”, World Economic Forum, 30 July 2015.

Farzana Badat, “The Philosophy behind Twin Peaks”, Twin Peaks Newsletter, Issue 1: The South African Perspective, The Financial Service Board, 2016.

South African Government, “South African Reserve Bank on Prudential Authority”, SA Government Communications, 1 Mar 2018.

Kirsten Kern, “South Africa: Twin Peaks Model of Financial Regulation”, Bowmans, 19 April 2018.

André Roux, “The Nationalisation of the SA Reserve Bank”, Stellenbosch Business School, 2 July 2018.

Vishnu Padayachee, “South African Reserve Bank Independence: The Debate Revisited”, Transformation, No. 89, 2015.

Media Relations, “SARB Statement on Nationalisation”, South African Reserve Bank Press statement, Thursday, 21 December 2017.

Jannie Rossouw, “Explainer: South Africa’s Central Bank – Ownership, Mandate and Independence”, The Conversation/Polity, 24 January 2019.

Alex Mohubetswane Mashilo, “The South African Reserve Bank Mandate”, The South African Communist Party, 5 June 2019.

Cobus Vermeulen, “On the Mandate, Ownership and Independence of the South African Reserve Bank”, South African Journal of Economic and Management Sciences, Vol. 23, No.1, 2020.

South African Reserve Bank, “Our Hundred-Year Journey”, South African Reserve Bank (SARB), 2021.

Cobus Vermeulen, “One Hundred Years of Private Shareholding in the South African Reserve Bank”, Economic History of Developing Regions, Vol. 36, Issue 2, June 2021.

Ntando Thukwana, “Kganyago Roots for Sarb Independence”, Bloomberg, 6 February 2024.

SA Legal Academy, “EFF’s SARB Amendment Bill Opened for Written Submissions”, SA Legal Academy, 13 June 2025.

Yeshiel Panchia, “Currency of Credibility – Sarb Nationalisation Debate in Parliament Opens a Legacy Hornet’s Nest”, Daily Maverick, 2 July 2025.

Bloomberg, “Treasury Rejects Reserve Bank Nationalisation”, BusinessTech, 2 July 2025.

Aurelia Mouton, “Expropriation Without Compensation: Treasury Against Malema’s Push to Nationalise Reserve Bank”, News24, 2 July 2025.

Babalo Ndenze, “National Treasury rejects attempts to reform and nationalise SARB”, Eyewitness News, 2 July 2025.

Babalo Ndenze, “Malema’s Private Member’s Bill To Nationalise SARB Gets Mixed Reaction During Public Hearings”, Eyewitness News, 2 July 2025.

Mark Bechard, “Government Opposes Taking Full Ownership of the Reserve Bank”, Moonstone, 3 July 2025.

Deborah Carmichael and Katleho Ntahale, “Guardians of the Rand: Potential Nationalisation of the South African Reserve Bank”, Ensight, 9 July 2025.

Articles & Insights, “South African Financial Sector Regulators: Who’s Who — FSCA, PA, SARB, FIC, NCR, Information Regulator (and more)”, Webmaster, 7 October 2025.

South African Reserve Bank, “Annual Report 2024/25”, South African Reserve Bank (SARB), 2025.

Mbulelo Mandlana, “Statement on SARB Repo Rate Hike: Finance Capital’s Assault on the Working Class”, Media Statement of the South African Communist Party, 29 May 2026.

Castro Khwela

Good morning fellow Compatriots!🙏🏾✊🏾👊🏾

Discover more from CASTRO KHWELA

Subscribe to get the latest posts sent to your email.